Client Lifecycle Management

CLM is now an essential banking infrastructure

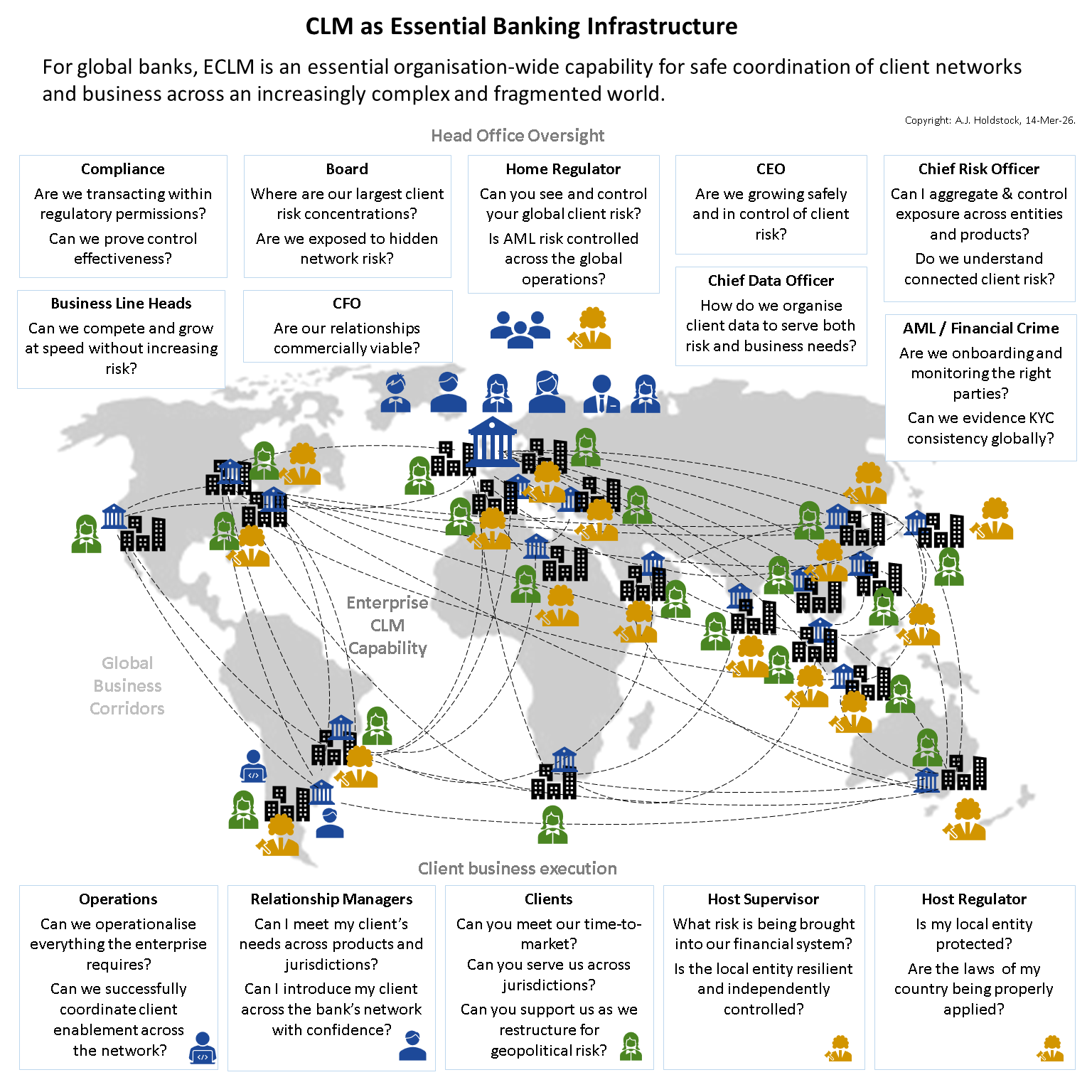

Modern banking depends on the ability to manage client relationships safely across complex legal, regulatory, and operational environments.

That capability increasingly sits within CLM.

Strong CLM enables growth, control, and adaptability.

Weak CLM creates friction, delay, rising cost, fragmented control, and avoidable risk across the organisation.

Why CLM Matters

Client business has become significantly harder for banks to manage safely.

Relationships now span multiple legal entities, jurisdictions, products, booking models, and regulatory obligations at the same time. What once sat within separate operational processes increasingly has to work together across the full client lifecycle.

Banks are expected to grow while maintaining confidence in:

who the client is

what business is permitted

where it can be booked

how risk is being managed

and how quickly changing conditions can be identified and responded to

Strong CLM makes this manageable.

Weak CLM creates operational friction, rising cost, slower client delivery, and growing pressure across the organisation.

Most importantly, it becomes progressively harder to adapt as complexity increases.

Many banks are still operating CLM structures designed for a much simpler environment.

What CLM Must Do

CLM exists to make client business possible under control.

In practice, that means coordinating onboarding, client data, regulatory obligations, risk assessment, lifecycle change, and operational execution across the enterprise at the same time.

It must:

enable client onboarding and activation

maintain trusted client and relationship data

manage change across the lifecycle

support risk and regulatory decision-making

coordinate requirements across products, jurisdictions, and booking entities

When these capabilities work together, banks can grow with greater control and less operational friction.

When they do not, banks experience delay, duplication, inconsistent decisions, operational friction, and rising cost across the organisation.

→

How CLM Works

CLM works through the coordination of data, process, controls, technology, and operational decision-making across the client lifecycle.

At the centre is the ability to maintain a reliable understanding of:

the client

their structure and relationships

the business being conducted

the obligations attached to it

and how those conditions change over time

Around that sits the operating system required to manage the lifecycle:

onboarding

periodic review

maintenance and change events

risk assessment

policy execution

operational workflow

governance and escalation

These components do not operate independently. Decisions in one area affect workload, data quality, risk exposure, client experience, and operational capacity elsewhere.

Strong CLM is therefore not built around individual processes or platforms alone. It depends on how the overall system behaves under pressure.

→

Why Many Banks Still Struggle with CLM

Most banks did not design CLM as a single integrated capability. It evolved over time in response to regulation, growth, product expansion, remediation, platform change, and local operational pressures.

As a result, many organisations now operate with:

fragmented ownership across business, operations, risk, and technology

inconsistent processes between regions or products

duplicated controls and manual workarounds

platforms carrying structural and data limitations

growing operational complexity layered over older models

Each individual change may appear reasonable. Over time, the overall system becomes harder to manage, harder to scale, and harder to change safely.

Many recurring CLM problems are symptoms of accumulated operational and structural complexity rather than isolated process failures.

→

What Good Looks Like

High-performing CLM is intentionally designed as an enterprise capability rather than a collection of disconnected processes and controls.

It combines:

clear accountability across business, operations, risk, and technology

trusted client and relationship data

coordinated lifecycle services across onboarding, review, and maintenance

controls embedded into operational execution rather than layered around it

consistent standards with flexibility where genuinely required

measurable performance across flow, quality, risk, and client outcomes

Strong CLM allows banks to absorb growth, regulatory change, and operational complexity with far less disruption than weaker operating models.

It creates greater institutional coherence across business, operations, risk, and technology.

Teams spend less time managing friction, remediation, and workarounds, and more time enabling client business under stronger control.

At that point, CLM becomes more than a control function. It becomes part of the bank’s operational infrastructure.

CLM, Risk & Resilience

Banks are operating in a more fragmented and unpredictable environment than they were a decade ago.

Geopolitical tension, sanctions expansion, regulatory divergence, and increasingly complex client structures are changing how institutions assess risk and maintain confidence in who they are doing business with.

In that environment, CLM becomes far more than an operational process.

It is the capability that helps the bank:

understand client structures and relationships

identify changing risk exposure

respond to regulatory and geopolitical change

maintain control across jurisdictions and booking models

and continue supporting client business safely under changing conditions

This is not simply a compliance problem. It is about protecting the institution while continuing to operate and grow in a more volatile world.

That is why CLM increasingly sits within broader conversations around resilience, control, and long-term strategic stability.

→

How Better CLM Is Built

Better CLM is rarely achieved through technology replacement alone.

High-performing capabilities are intentionally designed across operating model, data architecture, lifecycle services, controls, governance, workflow, and performance management so that the overall system can operate effectively under real operational conditions.

That requires difficult design choices:

where standards should be global and where flexibility is necessary

how client and relationship data is structured and governed

how operational flow and control interact

how accountability is distributed across business, operations, risk, and technology

and how the organisation absorbs growth, regulatory change, and increasing complexity over time

Many transformation programmes improve individual components while leaving the underlying structural problems largely intact.

Strong CLM emerges when the capability is designed deliberately as part of the bank’s operational infrastructure rather than treated as a collection of separate processes and platforms.

This site explores practical frameworks for doing that.

→

What This Site Focuses On

This site focuses on CLM as an operating capability: how banks establish, manage, control, and scale client relationships in increasingly complex environments.

The emphasis is not on covering every aspect of AML, KYC, or regulation in depth. Many specialist sources already do that well.

Instead, the focus here is on the areas where banks often struggle most:

operating model design

lifecycle coordination

data and relationship structures

onboarding and periodic review performance

governance and accountability

transformation complexity

and how CLM behaves under real operational pressure

The perspective throughout is practical rather than theoretical.

Most organisations already understand the individual components of CLM. The greater challenge is making the overall capability work consistently across products, jurisdictions, systems, and control functions as complexity increases over time.

That is the problem space this site explores.

A Practitioner Perspective

CLM is often approached through regulation, workflow, or technology in isolation.

In practice, the harder challenge is creating operational coherence across the enterprise as complexity, scale, and change increase over time.

The perspective throughout this site is shaped by operational, transformation, and design experience across large banking environments where client lifecycle management must function under real commercial, regulatory, and organisational pressure.

The focus is therefore less on theory and more on how CLM behaves under real operational conditions: where friction emerges, why transformation becomes difficult, and what stronger capability design looks like in practice.